Banks, NBFCs, insurance providers, lending platforms, and credit card businesses across India deal with a familiar operational strain: a steady volume of repetitive customer inquiries that doesn’t fit neatly into business hours, and support teams that can’t realistically scale headcount every time inquiry volume rises.

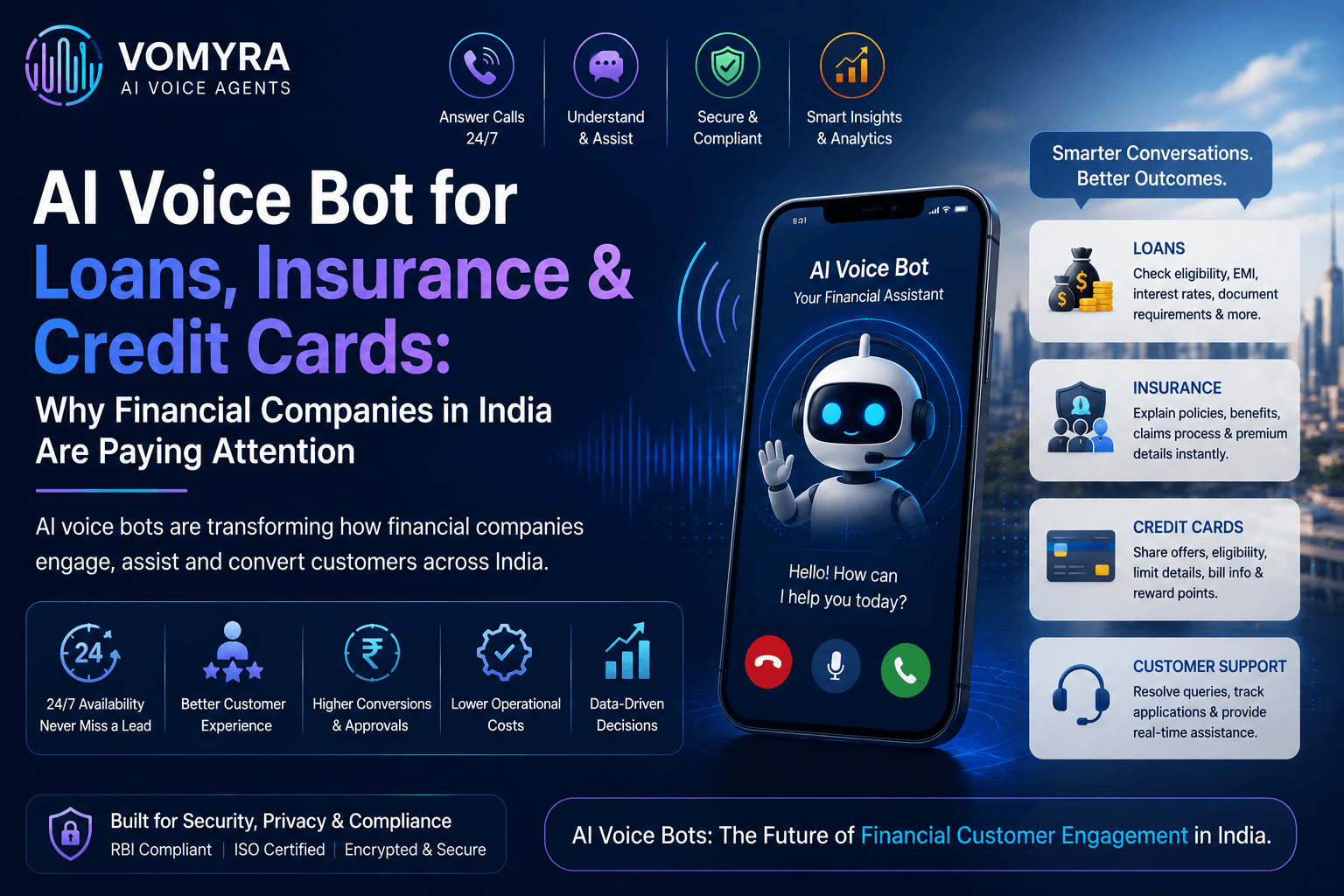

An AI voice agent for fintech in India is built to absorb that repetitive layer, answering questions about loan eligibility, policy coverage, and card offers the moment a customer calls, rather than asking them to wait for a callback the next morning.

This isn’t hypothetical. Major banks and digital lenders already use voice AI for loan-related conversations, and lending platforms use it for EMI reminders and renewal nudges.

The shift is happening because customer expectations around immediate answers have moved faster than most support teams can hire for, and because the kind of question a financial customer asks is, more often than not, one the company has already answered a thousand times before.

What an AI Voice Bot Actually Does

An AI voice bot is software that holds a real conversation with a customer over a phone call, rather than routing them through a fixed menu of touch-tone options.

A customer can ask what the interest rate on a personal loan looks like, whether they’re eligible for a particular product, what documents are needed, or when their next payment is due, and the system understands the question and responds in something close to a normal conversation.

It isn’t flawless, and it isn’t meant to replace a financial advisor for a complex discussion, but for the routine question that makes up most inbound call volume, it works well enough to matter.

Why Financial Services Generate So Much Call Volume

Money decisions come with questions, and lots of them. Someone considering a personal loan wants clarity before applying, an insurance customer needs coverage explained in plain terms, and a credit card applicant is comparing fees and eligibility across two or three providers at once.

Multiply that across thousands of customers in dozens of cities, and inbound volume becomes substantial even for a mid-sized lender, much of it falling into recurring categories: loan eligibility checks, EMI questions, policy renewals, application status, and KYC requirements.

Most of these conversations matter to the customer but aren’t actually complex, which is precisely what makes them suitable for AI-assisted handling instead of tying up a trained advisor’s time on a question already answered a hundred times that week.

The Cost of a Missed Financial Lead

Financial businesses spend meaningfully on customer acquisition, whether through paid search, social campaigns, or partner networks, which makes a missed inquiry more expensive than it looks on paper.

A customer filling out a loan inquiry form late at night, with a sales team planning to follow up the next morning, is a customer another lender may have already called back within minutes. In lending and insurance specifically, the company that responds first often wins the conversation, regardless of who has the better product underneath it.

How AI Voice Bots Support Lending, Insurance, and Card Businesses

For loan companies, an AI voice agent can run initial lead qualification the moment an inquiry comes in, asking about loan type, income range, location, and employment status before the lead reaches a human advisor.

Personal loan inquiries, which generate high volumes of repetitive questions about rates and eligibility, suit this automated first pass well, with qualified leads then routed to an advisor for the parts of the conversation that actually need one.

Home loan inquiries follow a similar pattern but typically need more upfront detail, such as tenure options and documentation, before a human takes over.

Insurance companies use voice AI somewhat differently, weighted more toward renewals and policy information than lead qualification. A policyholder asking what’s covered or how much the premium costs gets an immediate answer rather than waiting on hold, and automatic renewal reminders help reduce accidental non-renewal.

Claims handling stays a supporting role rather than a primary one, guiding a customer through initial steps and document checklists before a human takes over the actual review, since claims decisions aren’t something AI should make independently.

Credit card businesses see similarly high volumes of repetitive interaction, including application questions, payment reminders, and offer communication. A potential cardholder can ask about fees or reward structures and get a clear answer immediately, while existing customers receive a reminder ahead of a due date instead of discovering a late fee after the fact.

Why This Is Gaining Traction in Indian Fintech Specifically

India’s fintech sector has scaled quickly, creating predictable operational pressures: large inquiry volumes, high acquisition costs, support teams that are hard to scale linearly, and a customer base increasingly expecting service in a regional language rather than English by default.

A lender or insurer running campaigns across five or six cities can generate thousands of inquiries over a single weekend, and the businesses managing that volume well are generally the ones responding within minutes rather than days.

Language coverage matters more here than in most sectors, since financial conversations involve sensitive numbers people are far more comfortable discussing in their first language.

A customer in Jaipur may prefer Hindi, someone in Chennai may prefer Tamil, and a business owner in Ahmedabad may be more at ease in Gujarati.

A multilingual AI calling bot that switches naturally between languages, rather than defaulting everyone into English, tends to produce better information capture simply because people share more accurately when they aren’t translating in their head first.

The Part Most Vendor Pages Skip: Regulatory Boundaries

Financial conversations in India sit inside a real regulatory framework, and any AI voice deployment that ignores this is building on shaky ground regardless of how good the conversation quality sounds.

If the business is a regulated lender, the RBI’s Fair Practices Code and Digital Lending Guidelines apply: calls need to identify the lender within the opening moments, disclose the call’s purpose, avoid pressuring language entirely, and operate within permitted calling hours rather than whatever time is operationally convenient. Insurance conversations fall under IRDAI’s disclosure norms, requiring clear communication of policy terms and a documented path to the insurer’s grievance redressal mechanism.

Layered on top of both is the DPDP Act’s consent and data-handling requirements, and TRAI’s registration rules for any business making outbound calls at scale.

None of this is a reason to avoid voice AI. A well-built system can enforce these rules more consistently than a large distributed calling operation, since the disclosures are built into the conversation flow rather than left to an individual agent’s memory.

But it does mean calling-hour controls, mandatory identification scripts, and consent logging matter just as much as how well a platform handles Hindi, particularly for any lending or collections use case.

AI Voice Bot vs Traditional Call Centers

The honest framing isn’t AI replacing people, since complex financial conversations, hardship cases, and real negotiation still need a human who can read the situation and adapt. The difference shows up in availability and consistency instead.

A call center operates within shift hours and queues; an AI voice bot answers immediately, around the clock, applying the same qualification logic to every call and supporting multiple languages without needing to staff separately for each one.

The goal is reducing the repetitive workload sitting on top of the support team, not removing the team itself.

What Financial Companies Should Look For in a Platform

A handful of criteria separate a platform actually ready for financial use from one that isn’t. Natural conversation quality matters, since customers shouldn’t feel trapped inside a rigid script. CRM and loan management system integration determines whether customer information flows into the systems a team already uses, rather than sitting in a separate dashboard nobody checks.

Built-in compliance controls, including calling-hour enforcement and mandatory disclosure language, should be a baseline rather than an add-on.

And a fast human escalation path is non-negotiable for any case beyond routine information, since financial distress and disputes are exactly where a person needs to take over quickly.

For businesses evaluating this category for the first time, a no-code AI voice agent platform that can be configured and tested without engineering work makes it easier to pilot a single use case, such as loan FAQ handling or renewal reminders, before expanding further.

Where This Is Headed

Customer expectations keep shifting faster than most support operations can hire for, and financial companies face simultaneous pressure to respond quickly, protect service quality, and manage cost. Voice AI won’t handle every customer interaction, and it shouldn’t try to.

What it’s increasingly handling well is the high-volume, low-complexity layer underneath: loan pre-qualification, basic policy explanation, EMI reminders, and the kind of question that doesn’t need a trained advisor’s judgment, just an accurate, immediate answer.

A business wanting to test this on a narrow use case can start with a free AI voice agent trial to see how qualification logic and language handling perform against real call volume.

Frequently Asked Questions

Is an AI voice bot legal for use in lending and collections calls in India?

Yes, provided the deployment follows RBI’s Fair Practices Code and Digital Lending Guidelines, including identity disclosure, permitted calling hours, and a documented grievance redressal path. The compliance obligation sits with the regulated entity regardless of whether the call was made by a human or an AI system.

Can an AI voice bot replace a financial advisor?

No. It handles routine interactions like FAQs, eligibility screening, and reminders well, but complex discussions and anything requiring real judgment still need a human advisor.

Does AI voice technology support Hindi and other regional languages?

Most platforms built for the Indian market support Hindi, English, Tamil, Telugu, Marathi, Gujarati, Bengali, and other regional languages, which matters significantly for comfort during financial conversations.

How does an AI voice bot help with loan lead qualification specifically?

It engages a new inquiry immediately, asks structured questions about loan type, income, and eligibility, and passes only qualified leads on to a human advisor, rather than leaving every inquiry to wait for a manual callback.